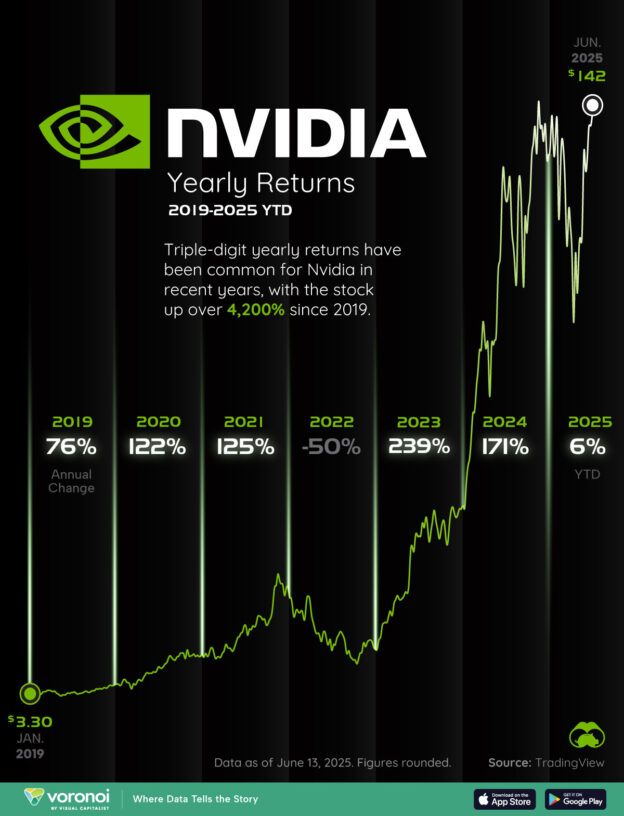

Riding the AI boom, Nvidia, at a market cap of $4 trillion, appears to have earned enough trust among power electronics and power system companies serving AI-driven data centers.

Many suppliers of Wide Bandgap (WBG) semiconductors and silicon vendors are playing along, willing to invest in new technologies to deliver what Nvidia needs.

Gerald Deboy, head of the System Innovation Group at Infineon Technologies, compared Nvidia to a maestro, orchestrating “the entire world to architect a new way of building and operating data centers.”

Those enlisted by Nvidia include Infineon, MPS, Navitas, ROHM, STMicroelectronics, Texas Instruments to advocate the transition to 800 V high-voltage direct current (HVDC) data center power infrastructure. Also in the mix are suppliers of power system components such as Delta, Flex Power, Lead Wealth, LiteOn, Megmee, and companies who build data center systems, including Eaton, Schneider Electric and Vertiv.

Hassan Cheaito, market and technology analyst in power electronics at Yole Group, sees Nvidia’s push for AI data centers is creating momentum behind Gallium Nitride (GaN) as like a “Tesla moment for SiC (Silicon Carbide).”

Just as STMicroelectronics reaped the fruits of Tesla’s early push for SiC, Infineon and Navitas are jockeying to profit from the emerging GaN moment driven by Nvidia.

Hybrid solutions

It’s clear why Nvidia demands this wholesale redesign.

As it rolls out its Rubin Ultra GPU and Vera CPU in 2027 and clusters as many as possible within a rack to keep pace with the growth of AI, Nvidia has turned away from 54V in-rack power distribution, designed for kilowatt (KW)-scale racks. That technology can’t cope with the growing per-rack power level required by the massive clustering of new GPUs.

Legacy rack power systems can’t handle the physical limitations created by space constraints and copper overload within a rack. Nvidia has recognized that repeated AC to DC transformations across the power chain aren’t energy efficient and increase failure points.

Hence, although its GPU business sits furthest from the power core, Nvidia is dictating a holistic redesign of the power infrastructure for AI data centers.

A plethora of new power devices and semiconductors will be needed for the new 800V High-Voltage Direct Current (HVDC) data center architecture.

Put simply, Nvidia wants the server board to run on 800-volt DC, making it necessary to convert from 800 volts down to the point of load voltage. Given space constraints, this won’t be easy. Infineon, for example, is building 800 volt to 12 volt, and 800 volt to 50 volt converters, to demonstrate the technology to Nvidia in power density, efficiency, form factors, height and so on.

So, what types of power devices are needed?

Infineon’s Deboy explained, in data center power infrastructure that needs high-power, high-voltage solutions, SiC leads. But for conversion from 800 to 50 volt, space restraints dictate high-switching frequency. This makes it “more of a GaN domain,” he added. Meanwhile, for conversion from 54 volt to six volt, in so-called low voltage intermediate bus converters (IBC), both GaN and silicon are okay.

Further, the new 800 V AI data centers also demand the invention of new semiconductor-based relays, explained Deboy.

In data centers today, AC is distributed in three phases, with a normal relay and a normal switch turning power on and off like a light switch. In contrast, in a new high-voltage DC AI data center, Deboy said that safety requires “new semiconductor components that control over currents and inrush currents in a very well-maintained behavior.”

Taken all together, Poshun Chiu, principal technology and market analyst at Yole Group tabbed Infineon as “by far the leader in power electronics.” When AI data centers ask for a hybrid power electronics solution, noted Chiu, Infineon’s strength shines in all three fields, ranging from SiC to GaN and semiconductors. Infineon, added Chiu, covers every phase of the power chain in AI data centers, striving to offer the best technology fit for each stage.

Infineon, however, isn’t alone in racing to capture Nvidia-driven AI data center opportunities. Gene Sheridan, CEO of Navitas Semiconductor (Torrance, Calif.) noted, “As you get closer to the processor, Nvidia gets more hands on.” Starting at 48 volts, Nvidia is driving design, component selection and supplier selection, he said. “We’re working with them every week…on evaluations, characterizations, benchmark testing, prototyping, to help Nvidia figure out that final solution.”

Navitas is taking advantage of its strength in GaN to address power electronics solutions required by AI data centers. The acquisition of GeneSiC Semiconductor in 2022 has also helped Navitas bolster its wideband gap IC portfolio.

Beyond GaN or SiC, useful for traditional AC to DC converters, or 800-volt DC to DC converters, Navitas also dabbles in “48 volt down to power the processor,” which is closest to the processor.

But Sheridan finds a new opportunity for GaN, triggered by the industry’s highest voltage SiC technology, which his company obtained via its GeneSiC acquisition. Ultra-high-voltage SiC technology will be essential in developing “solid state transfers” connected to the grid. Beyond data centers, Sheridan believes grids are getting upgraded to solid-state transformers everywhere, powering cities and homes, even connecting to renewable energy.

What about other hyperscalers?

By preemptively unveiling its plans for data center power infrastructure, Nvidia has successfully driven the industry conversation.

But unknown is that between now and late 2027, when Nvidia launches Rubin Ultra—in expectation of 800 V HVDC—how will Google and Meta respond?

Nvidia’s aggressive initiative could make the Open Compute Project (OPC) obsolete.

In the past, OPC led in standardizing form factors and rack levels for data centers. Today, “OCP is moving too slow,” said Infineon’s Deboy. Diverging architectures emerging in intermediate phases could send data centers back into “the jungle,” said Deboy, where none of the data center solutions will be compatible, like pre-OCP days.

That could put suppliers of power electronics devices to serve multiple hyperscalers with diverging roadmaps.

In the AI data center market, Yole Group predicts that GaN will outgrow SiC. While SiC is focused on AC to DC, GaN used in DC to DC can also enter AC to DC. This is because GaN devices pose the potential for higher voltage, explained Chiu. “Although we see some upside market for SiC, about $100 million in three to five years, the opportunity seems much bigger for GaN.”

https://www.yolegroup.com/strategy-insights/nvidia-defines-power-electronics-future/