The Indian real estate investment trust (Reit) market has attained significant maturity since the launch of the Embassy Reit in April 2019. The regulatory environment is making Reits more accessible and relevant. A few significant developments in the past few months include the issue of the third Reit by Brookfield, the follow-on issue by Embassy Reit, and major debt issuances by Embassy and Mindspace.

Reit has now established itself as a strong alternative financial platform to raise funds in the real estate sector. It is changing the way commercial real estate operates. The first Reit was listed only in 2019. Since then, two more Reits have been listed on the Indian bourses in most difficult business times, and many more entities are exploring the option. The success of Reits has created even stronger interest from global equity/sovereign/pension funds to invest in development assets as exit mechanism is now established. InvITs enable the developers of infrastructure assets to monetize their assets by pooling multiple assets under a single entity. These assets have long-term contracts that provide a steady cash flow for 15-20 years.

In June 2021, Sebi reduced the minimum investment amount in Reits to ₹10,000-15,000 from ₹50,000. It will also bring Reits at par with other equity traded instruments in the market. It will also improve liquidity due to higher trading, resulting in market price discovery.

The government has approved foreign portfolio investors to invest in the debt securities issued by Reits. This is a good move for Reits in India and will open a large funding source and create a broader base of financing for the sector. It will also make Reits in India more attractive to large foreign investors and improve investors’ confidence in the office sector. This also helps Reits raise higher debt at a competitive cost.

Reits are an attractive investment option for investors seeking to diversify their portfolio. The past two years have shown that Reits provide a stable return even in uncertain times. Investors can earn income through rentals received from properties owned by Reits which could be in the form of a) dividend income, b) interest income, c) redemption of capital and/or capital gains via sale of Reit units in the secondary market.

Listed Reits in India provide an annualized distribution yield return of 6-7%

• Reits are diversified and assets are spread across major regions such as Bengaluru, Mumbai, Hyderabad, NCR, Pune, etc

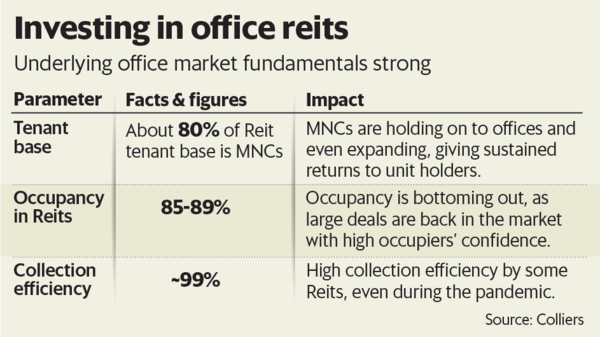

Reits can only invest in rent-yielding properties and more than 80% of the investment has to be in completed assets

• At least 90% of rentals received from invested properties have to be distributed to the unit holders

The underlying office market fundamentals are strong.

Reits have opened a large funding source for the real estate sector. They help developers focus more on executing realty projects and give them an option to monetize their rent-yielding asset and exit the property at its peak valuation. Reits have also been raising debt at lucrative rates from the market, reducing the overall cost of capital. In the past few years, they have been able to reduce their weighted average cost of debt to about 6.5-7% from over 9% at the time of its initial issue. Other Reits too are planning to raise debt. This will help reset the debt portfolio efficiently and benefit unitholders.

Overall, Reit regulations have become more investor friendly over the past two years. We are also seeing many global investors investing in office assets. They are looking to create a strong portfolio that will be Reit-ready.

Piyush Gupta is managing director, capital market and investment services, Colliers India.

https://www.livemint.com/money/personal-finance/reits-invits-are-emerging-asset-class-in-india-11640624330135.html