- I’m not against buying private real estate, as I have owned my fair share, close to $100 million (held in various partnerships) prior to 2010.

- While publicly listed REITs provide better liquidity and are ready-made for the average investor, private real estate can oftentimes be less volatile.

- Blackstone has a firm grasp of creating shareholder value and buying shares at the current level is what “intelligent investing” is all about.

According to the Stanger Report, non-traded NAV (net asset value) REIT returns outpaced those of publicly listed REITs with a cumulative total return of 70.1% over the last 60 months (vs publicly listed REITs that returned 58.5%). Kevin Gannon, chairman and chief executive officer of Stanger, explained,

“This performance highlights the benefits of a non-listed NAV REIT vehicle, that historically has provided a mostly steady real estate-based return without the extreme ongoing volatility of the traded market. This strong performance is the driving force behind $12.1 billion of NAV REIT fundraising in first quarter 2022, and we expect this trend to continue.”

According to Stanger, over the last 12 months, the top performing non-traded NAV REIT was Cottonwood Communities (Class A at 102.18%), and the top performing traditional lifecycle REIT was Resource REIT (67.12%).

Over a five-year period, Blackstone Real Estate Income Trust (Class I at 14.30% annualized) was the top performing NAV REIT, and Resource REIT (15.33% annualized) was the top performing traditional REIT. In related news, Stanger reported that fundraising for non-traded alternative investments hit $32.9 billion in the first quarter of 2022.

As I often tell my readers here on Seeking Alpha, I’m not against buying private real estate, as I have owned my fair share, close to $100 million (held in various partnerships) prior to 2010.

While publicly listed REITs provide better liquidity and are ready-made for the average investor, private real estate can oftentimes be less volatile, which of course is the primary attraction to the asset class.

Remember that one drawback to private real estate investing is that you must either invest directly (which is what I did) or find a suitable sponsor. That can be challenging however, as many private sponsors do not provide the same level of transparency as publicly listed REITs do.

There are literally hundreds of sponsors, ranging from crowdfunding, to accredited investors, to non-traded REITs, and I often tell others that you must always conduct your due diligence when investing in a real estate fund, and not just take their word for it.

Personally, I prefer to eat my own cooking, and invest in myself. With over 30 years of commercial real estate experience, I have found that my knowledge of certain sectors (like net lease and retail) are advantages so I can scoop up buildings without the need to pay asset management fees.

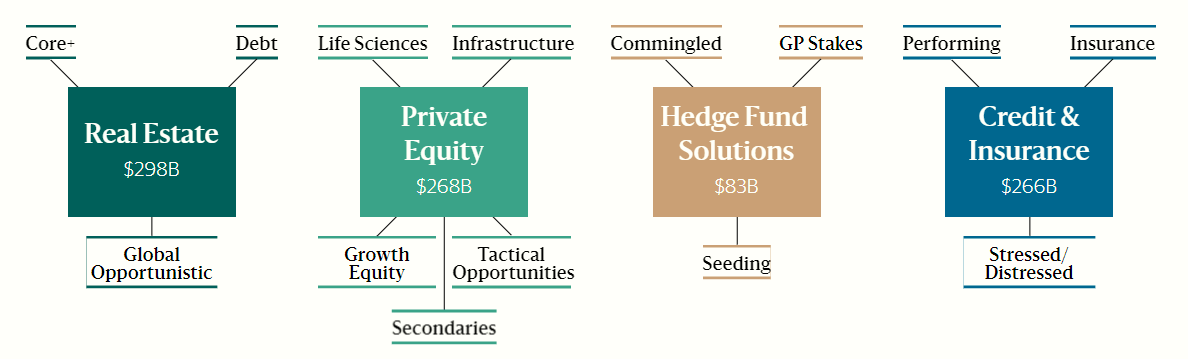

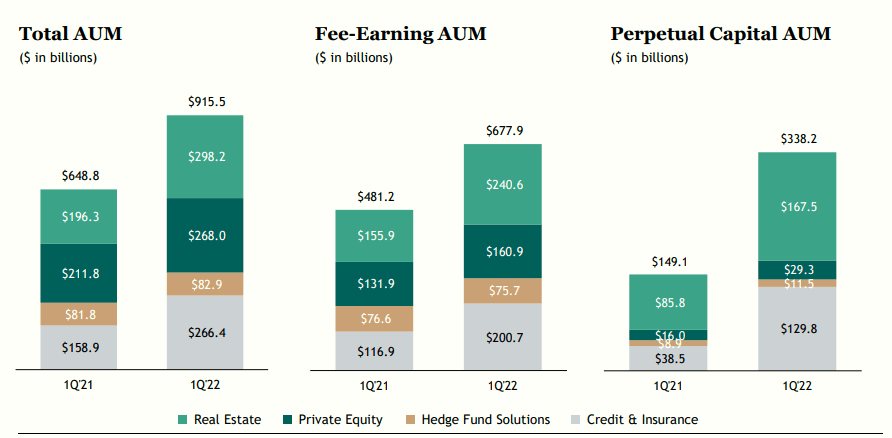

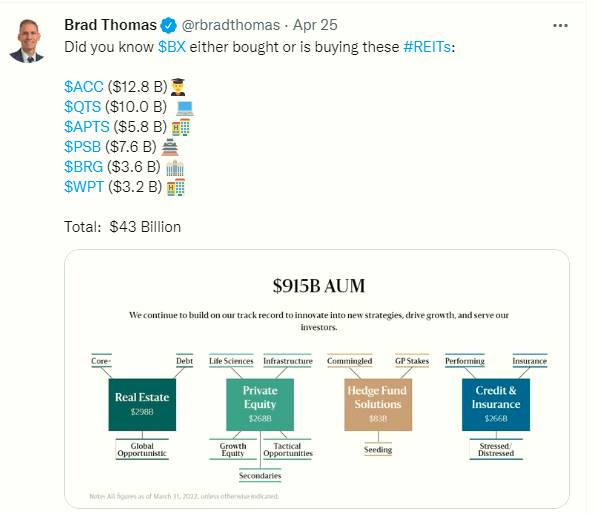

That being said, my wallet is simply not large enough to buy large portfolios, so instead of trying to get too big for my britches, I’m an investor in Blackstone Inc. (NYSE:BX), one of the world’s largest alternative asset managers with over $915 billion in assets under management including investment vehicles focused on private equity, real estate, public debt and equity, infrastructure, life sciences, growth equity, opportunistic, non-investment grade credit, real assets and secondary funds, all on a global basis.

BX Website

BX’s diverse assortment of funds makes private equity, real estate, credit, and hedge fund investments around the world, and the company also provides investment advice and management services to institutional investors through separately managed accounts.

On the recent earnings call (Q1-22), Stephen A. Schwarzman Chairman, CEO, and Co-Founder explained how BX differentiates itself from its peers,

“There are certain attributes that characterize a great financial firm, including strong investment performance over long periods of time, significant growth in assets while maintaining debt performance, the ability to continuously innovate, a trusted brand, loyalty from customers who themselves are healthy and growing, wide geographic and product reach, a distinctive high-performance culture, the ability to attract and keep great talent, and the capacity to identify and act upon paradigm shifts before others.

It is rare even for a great firm to possess several of these pillars of success. At Blackstone, I believe we have demonstrated we have all of them.”

That Says It All, Doesn’t It?

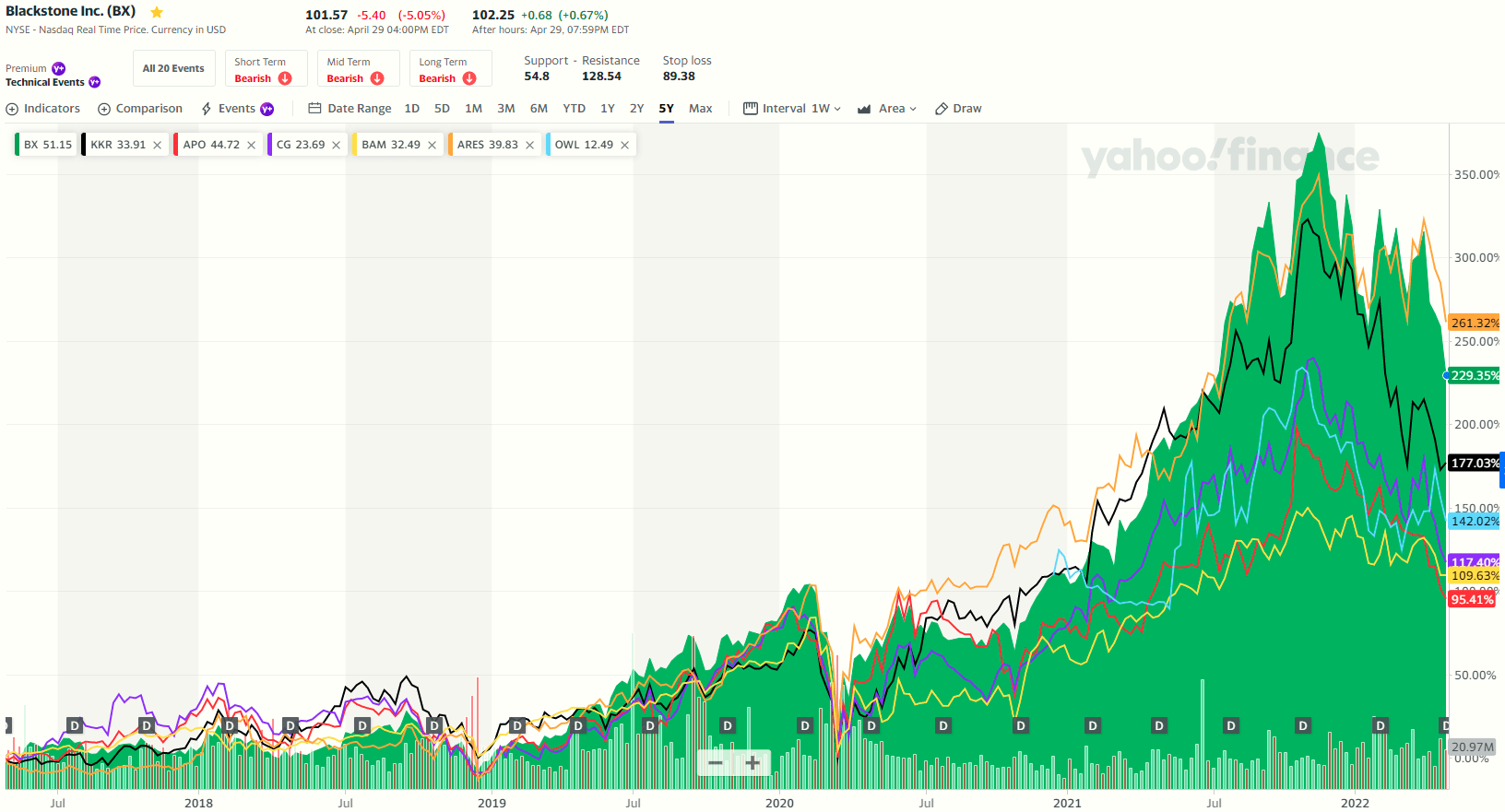

As the largest alternative manager in the world, BX has built leading businesses across all of the major asset classes with uniformly outstanding returns. Its flagship strategies have significantly outperformed the comparable public indices, including 16% to 17% net returns annually, corporate private equity and global opportunistic real estate for three decades, leading the indices by approximately 5% to 9% per year.

Yahoo Finance

In Q1-22, BX’s real estate business, its largest business, delivered superior sector returns of around 9%. Just in Q1-22 inflows reached $50 billion and $289 billion for the last 12 months.

Over the past 3 years, the firm generated $500 billion of inflows, which is greater than the total AUM of any other alternative firm.

You may recall that I wrote an article back in 2019 in which I explained that BX was removing certain restrictions by eliminating its K-1 tax forms. This allowed everyday investors to receive 1099s while getting rid of effective connected income (“ECI”) and unrelated business income tax (“UBTI”).

“This made it possible for the stock to become eligible for inclusion on CRSP, MSCI, and Total Market indices. By officially converting to a corporation on July 1, 2019 – thereby unhampering long-only and index/ETF investors – Blackstone said it could double in size to $9 trillion.”

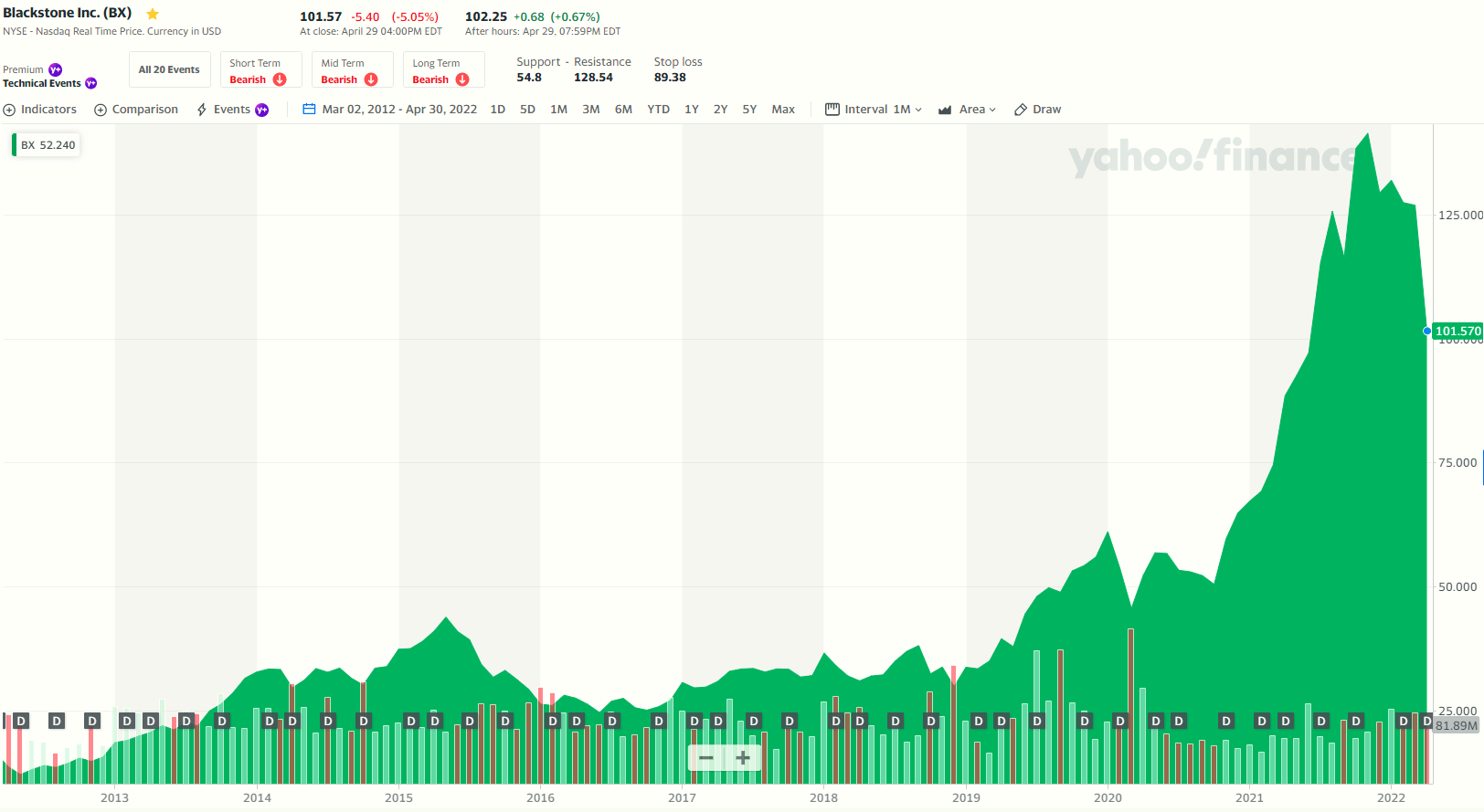

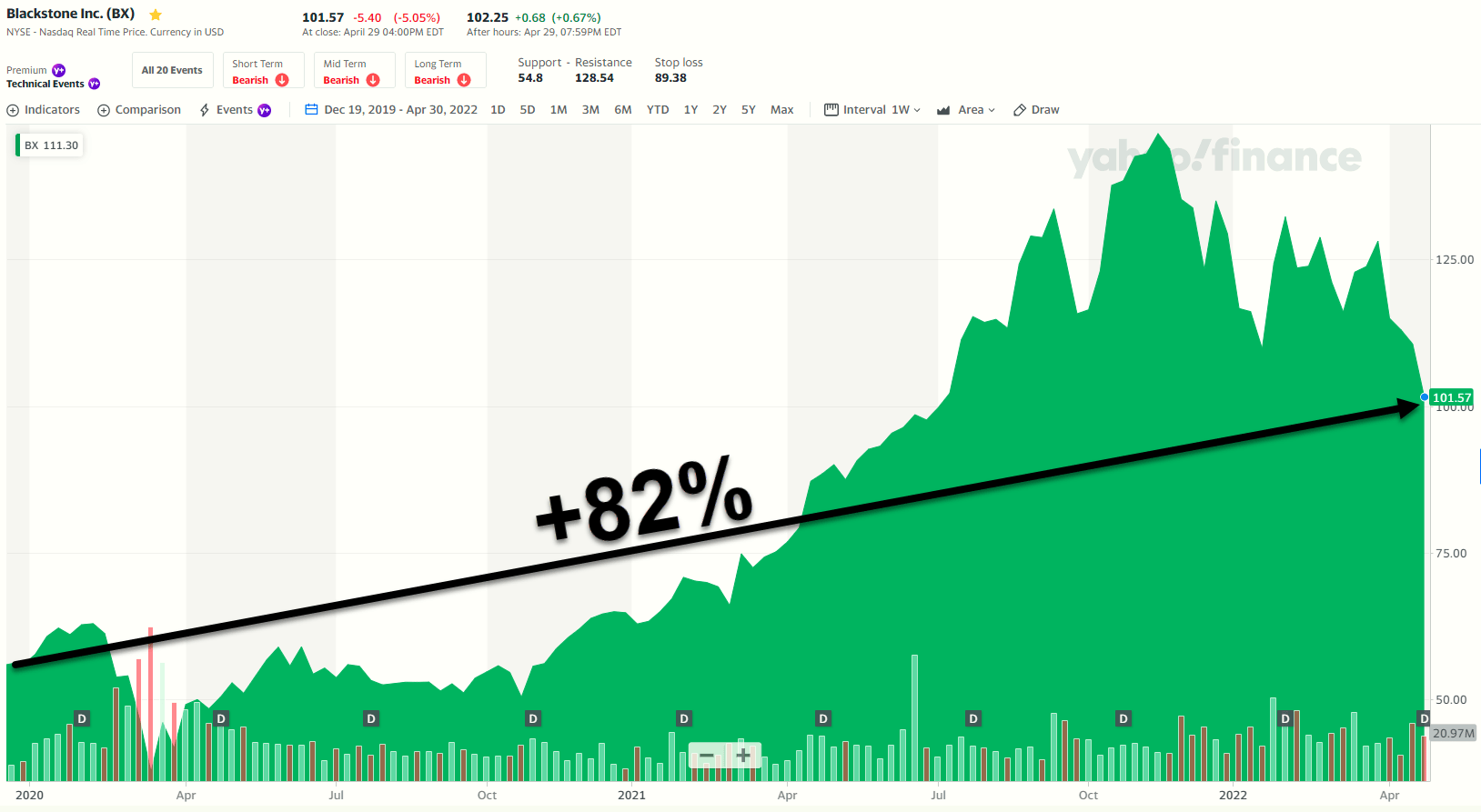

Since 2019, shares are up over 82%, even after a sell-off that commenced in 2022.

Yahoo Finance

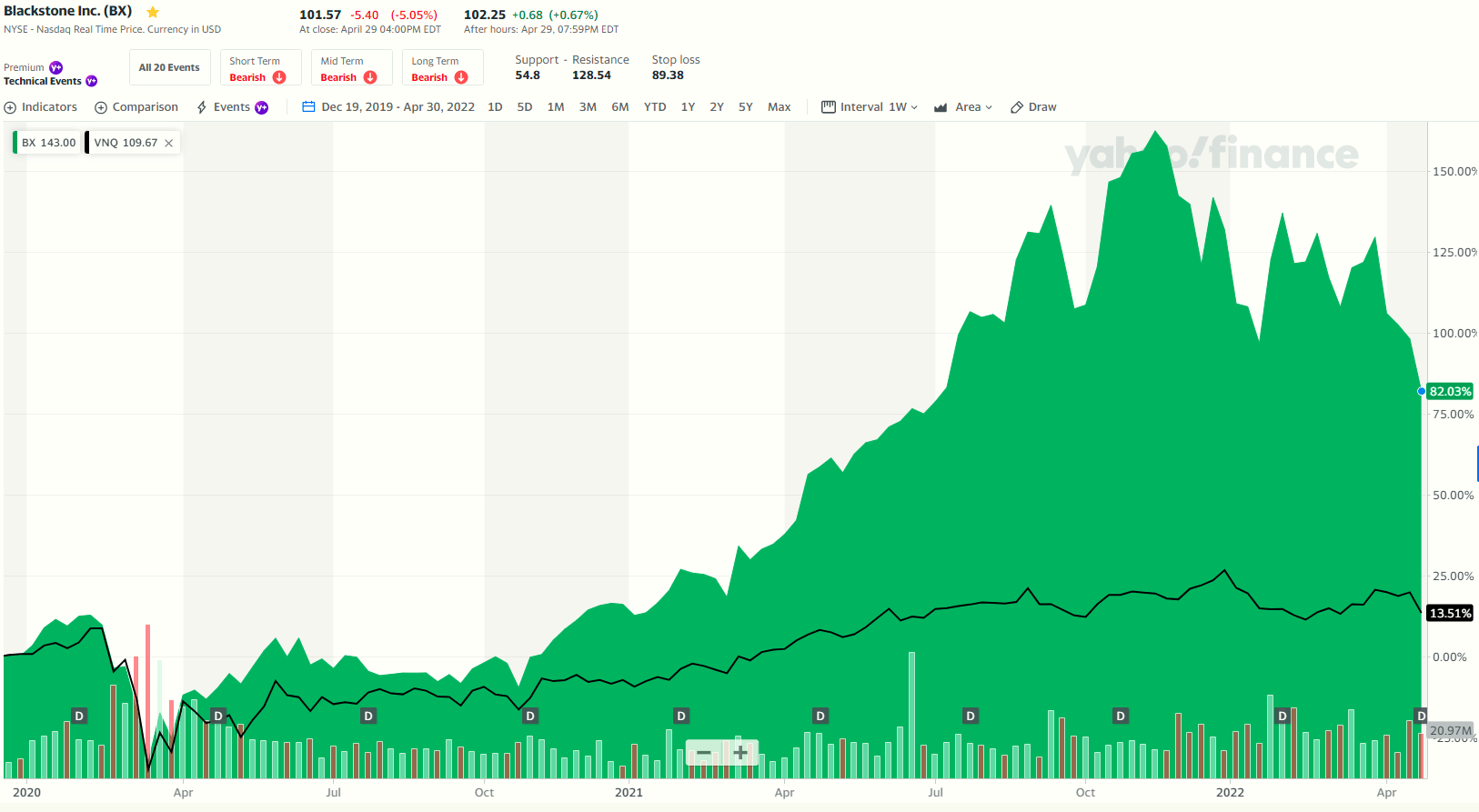

Not bad, especially when you compare that performance with REITs – as seen below we’re using the Vanguard Real Estate ETF (VNQ) as the REIT benchmark:

Yahoo Finance

What about direct peers?

Yahoo Finance

As you can see, Ares (ARES) is the only peer that has outperformed BX, while all of the other underperformed: KKR & Co. (KKR), Apollo Global Management (APO), The Carlyle Group (CG), Brookfield Asset Management (BAM), and Blue Owl Capital (OWL).

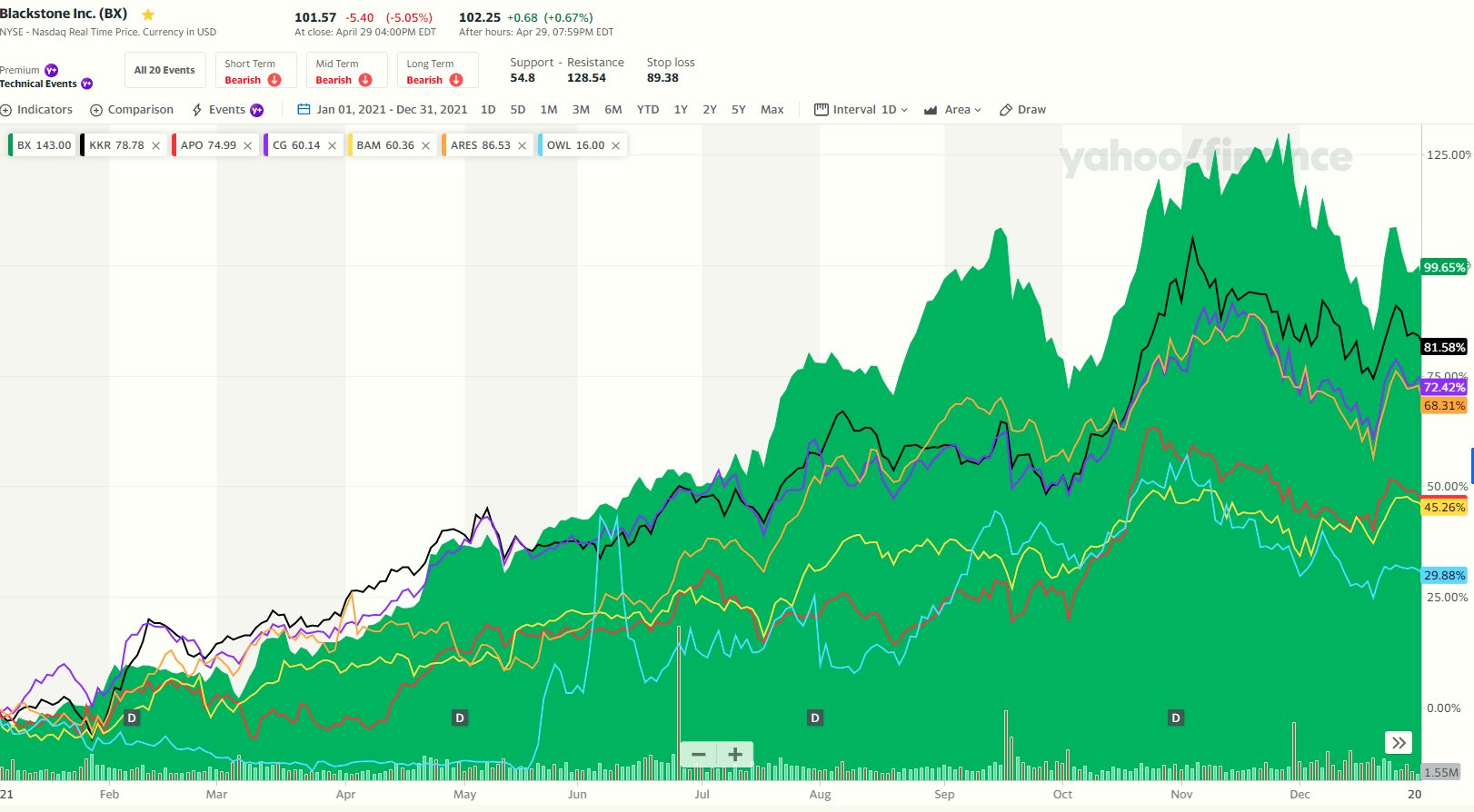

Blackstone’s The Most Consequential Year

In the Chairman Letter, Stephen Schwarzman explained,

In 2021 BX’s Distributable Earnings rose 85% year-over-year to $6.2 billion, while Fee Related Earnings (“FRE”) increased 71% to $4.1 billion over the same period. In terms of investment performance – the foundation of our business – we achieved record total appreciation across our funds. Our opportunistic real estate and corporate private equity funds both posted their best annual returns in over a decade, appreciating over 40%.

When we deliver great returns to our customers, it creates a virtuous cycle, building trust and leading to further inflows. Our limited partners entrusted us with a remarkable $270 billion in 2021, lifting assets under management by 42% to an industry-record $881 billion.

At our September 2018 Investor Day, we outlined a path to $1 trillion of AUM in eight years, and we now expect to surpass this milestone this year – in roughly half the time we predicted. 2021 represented the most consequential year in Blackstone’s 36-year history.“

Yahoo Finance

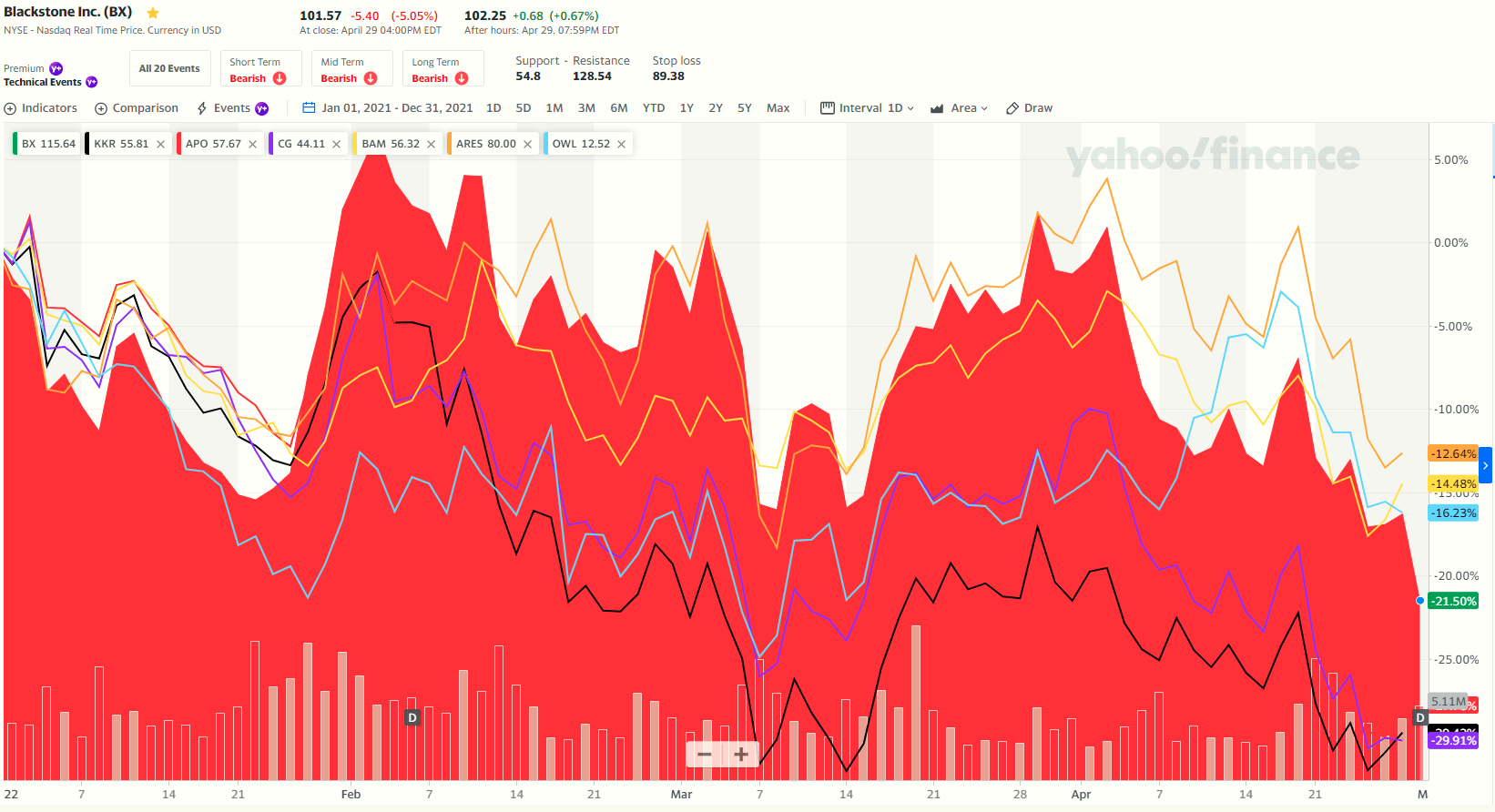

As seen above, BX was certainly the top private equity player in 2021; however, 2022 is a different story as shares have slid by 21%, ranking BX in the middle of the pack in terms of its direct peer group.

Yahoo Finance

Let’s now take a closer look at BX’s latest (Q1-22) earnings results…

Blackstone’s Latest Earnings Results

One of the most significant developments in 2021 was BX’s accelerated expansion into the retail and insurance channels.

In retail, which represents an $80 trillion addressable market today, BX has established itself as a leading alternative business with non-traded REIT (“BREIT”) and BDC (“BCRED”).

BX has continued to raise a total of $4 billion to $5 billion per month of equity capital for its three retail perpetual vehicles: BREIT, BCRED and BEPIF, including the most recent monthly subscription on April 1st.

Investors recognize BX’s products are well positioned for the inflationary environment, given BREIT’s focus on hard assets with short-duration leases, while BCRED is a floating rate vehicle with an average loan-to-value of 43%.

BREIT more than doubled in size year-over-year to $63 billion, generating 5.8% appreciation in Q1-22. BX has a powerful brand in the retail channel and an enormous first-mover advantage, selling products today through a broad network of distribution partners.

In the insurance business, AUM has more than doubled year-over-year to $155 billion. Last year BX was named the external manager of a significant portion of AIG’s Life and Retirement portfolio, one of the largest U.S. life insurers. BX also took over asset management of a life insurance and annuity company from Allstate in a new Blackstone-managed vehicle.

BX’s strategy is to attract third-party asset management contracts with high-quality insurance clients – not to become an insurance company or take on its liabilities.

Q1-22 BX Investor Deck

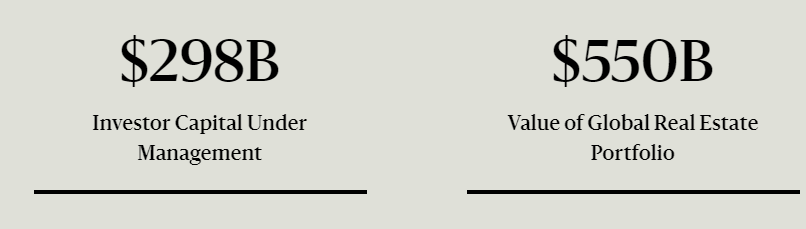

As seen above, BX’s largest AUM-driver is real estate, and as of Q1-22, the company’s global real estate portfolio was valued at $550 Billion. Keep in mind, that’s around 20% of the entire asset value of the publicly listed REIT sector.

BX Website

BX has been extremely active in acquiring logistics properties, that comprise 40% of the portfolio. BX first started investing in this sector at scale in 2010 given the expected explosion in e-commerce and today it owns approximately $170 billion of warehouses. As I pointed out on Twitter recently, BX has been opportunistic in acquiring public REITs, such as American Campus (ACC) for $13 billion and Preferred Apartment Communities (APTS) for $6 billion.

Twitter @rbradthomas

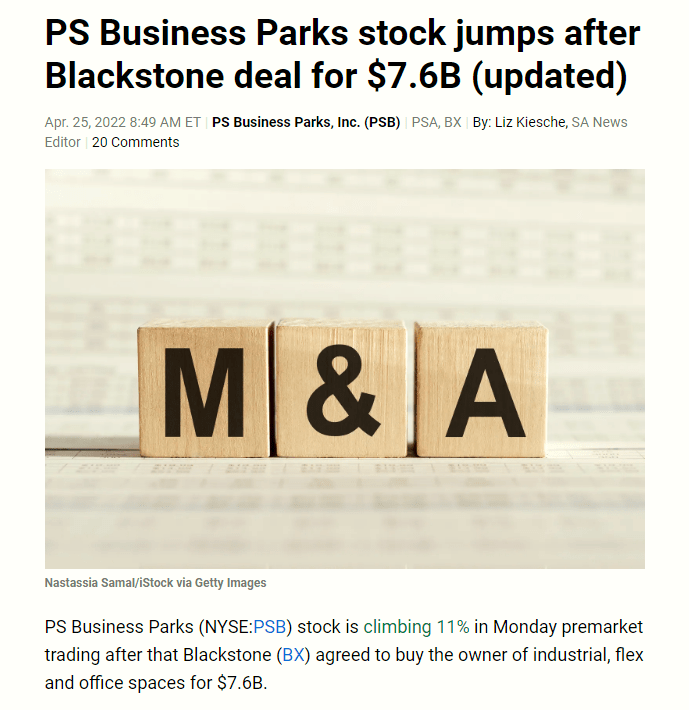

Other REITs acquired by BX include QTS Realty ($10 billion), BRG ($3.6 billion), and WPT Industrial ($3.2 billion). More recently the company announced the acquisition of PS Business (PSB) for $7.6 billion.

Seeking Alpha

Let’s not forget BX’s acquisition of BioMed ($14.6 billion), Excel Realty Trust ($1 billion), and Extended Stay America – along with Starwood ($6 billion). BX seeks to deploy capital in areas where it has a high conviction such as: Rental housing (Home Partners of America, APTS), Digitalization of the economy (QTS data centers and Hotwire Communications), and Logistics.

The Power Of Scale

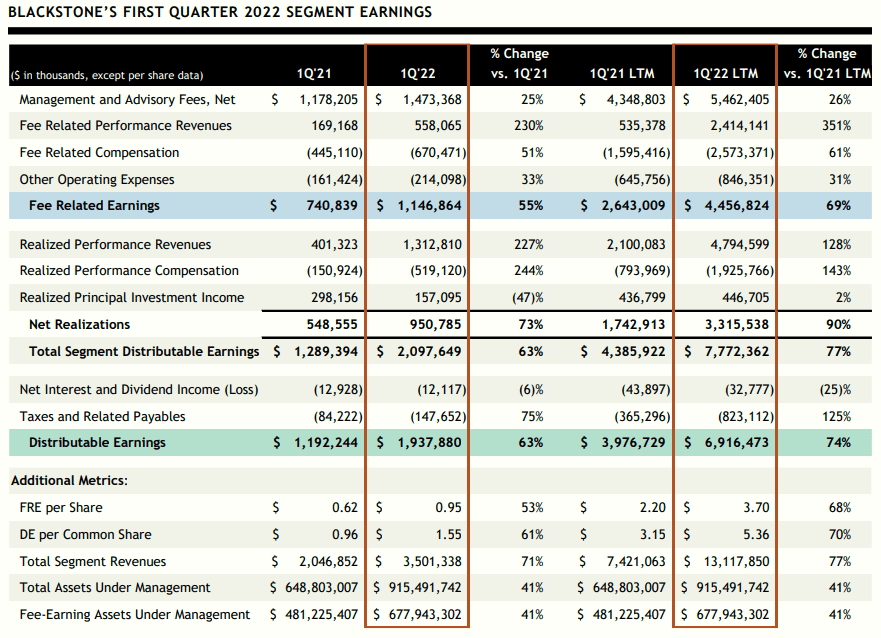

BX has a great first quarter representing one of the two best in the company’s 36-year history. Distributable earnings in Q1 rose 63% (year over year) to $1.9 billion, while fee-related earnings increased 55% to $1.1 billion.

Q1-22 BX Investor Deck

Fund realizations reached a record $23 billion and included the refinancing of BX’s U.S. logistics portfolio, the partial sale of fintech company, IntraFi, and the monetization of stakes in various private and public holdings across the firm.

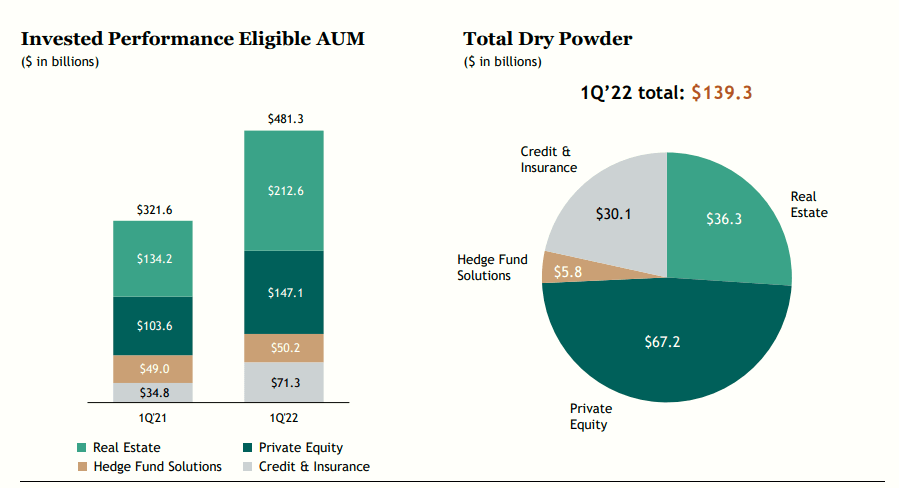

The dramatic expansion in the number and scale of the firm strategies and commensurate increase in aggregate deployment has led to a record $481 billion of performance revenue eligible value in the ground, up 50% year-over-year.

Q1-22 BX Investor Deck

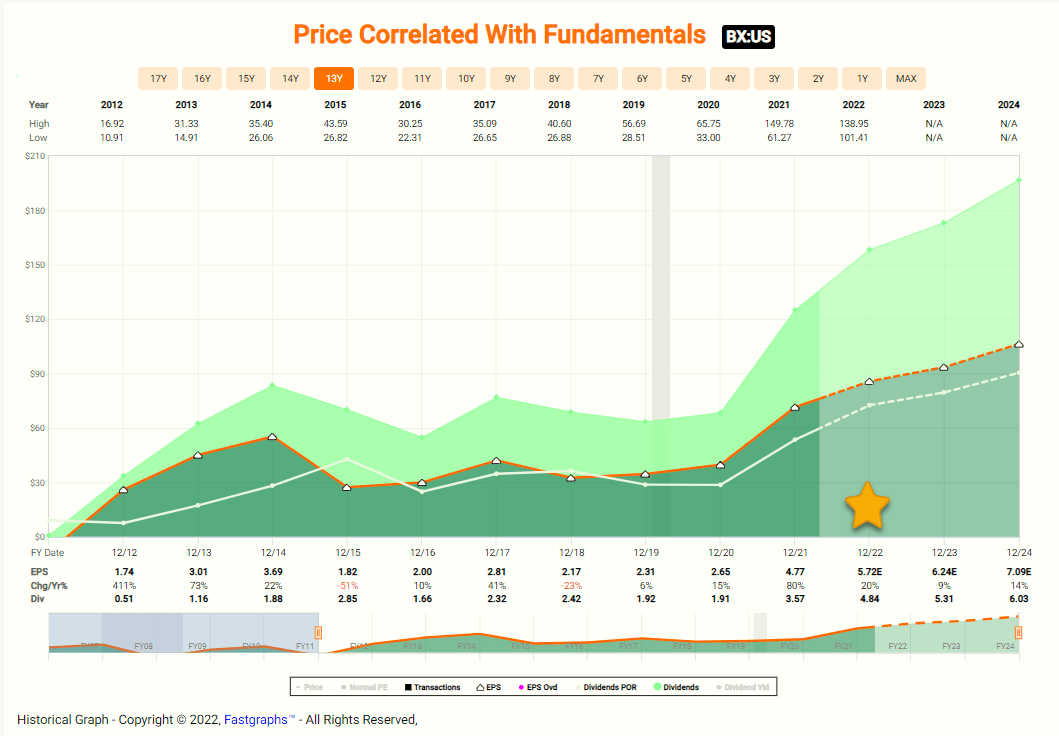

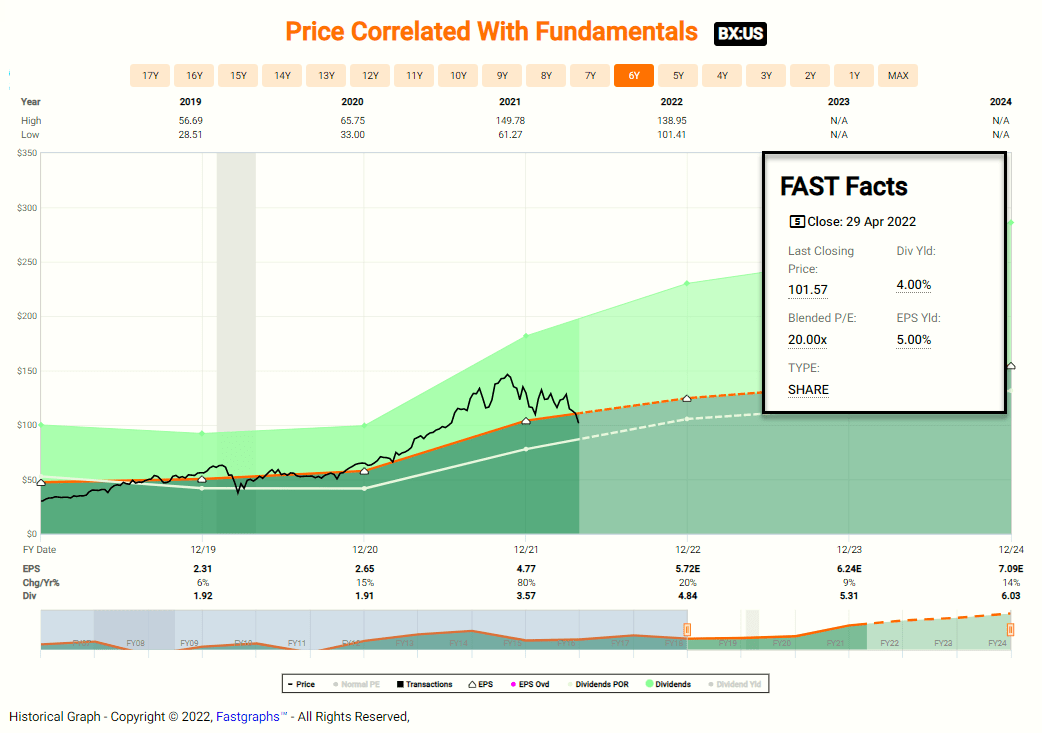

At the same time, sustained investment outperformance across the platform on this growing base of invested capital has driven a continued expansion of the firm’s store value. As seen below, analysts estimate BX’s EPS of $5.72 in 2022, an increase of 20% from 2021.

Fast Graphs

BX is on a path to hit $1 trillion of AUM in 2022 and ultimately well beyond with commensurate significant elevation in earnings power and earnings quality.

BX Website

BX has declared a quarterly dividend of $1.32 per share that will be paid on May 9th. $1.7 billion is to be distributed to shareholders with respect to Q1-22 and $7.2 billion over the LTM through dividends and share repurchases.

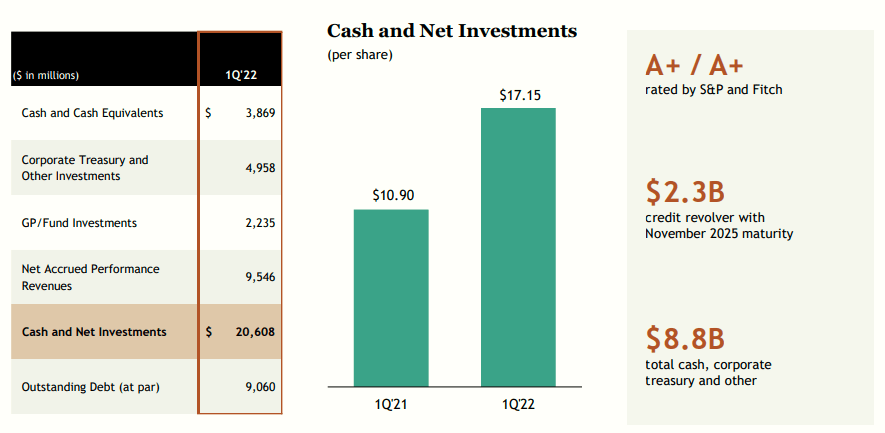

As of Q1-22, BX had $8.8 billion in total cash, cash equivalents, corporate treasury, and other investments and $20.6 billion of cash and net investments, or $17.15 per share. It has a $2.3 billion undrawn credit revolver and maintains A+/A+ ratings.

Q1-22 BX Investor Deck

Who’s Buying Buy BX Stock?

As viewed below, BX shares are now in our “buy zone” trading at $101.57 with a P/E multiple of 20x. The dividend yield is 4.0%.

Fast Graphs

Compared to the peers:

- ARES: 23.7x and 3.7%

- KKR: 11.7x and 1.1%

- APO: 10.3x and 3.2%

- CG: 7.7x and 3.6%

- BAM: 13.6x and 1.1%

- OWL: 29.0x and 3.4%

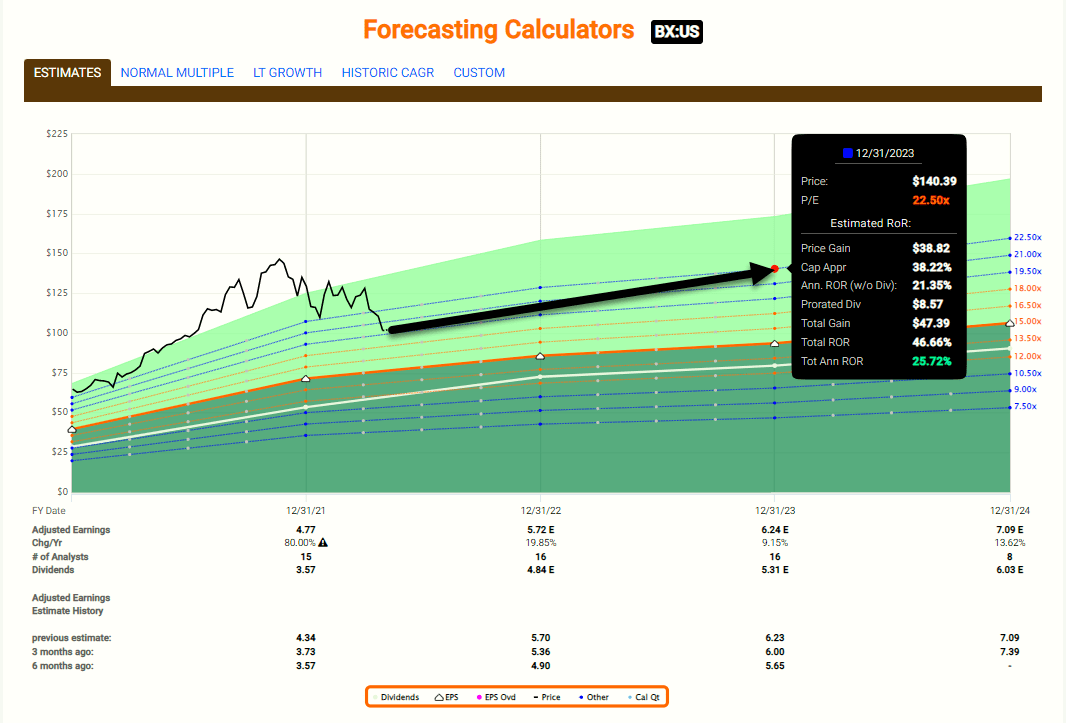

So BX is the highest yielding firm in the peer group and beyond 2022 analysts are modeling growth (average) in 2023 and 2023 of around 10%. Using the FAST Graphs forecasting tool (below) we model BX to return 25% annually:

Fast Graphs

Once again, one of the key differentiators for BX is its first mover advantage in the non-traded real estate sector and with the fear factor (rising rates and inflation) we’re witnessing in the public sector, it makes perfect sense for BX to provide an alternative product line that compliments its core multi-lever strategies.

BX has a terrific understanding of the REIT business model, as it’s the quintessential candle that burns at both ends – acquiring cheap publicly listed REITs and incubating soon to be listed REITs. The company has a firm grasp of creating shareholder value and buying shares at the current level is what “intelligent investing” is all about.

https://seekingalpha.com/amp/article/4505616-blackstone-strong-buy-private-equity-juggernaut