There is a need to create a robust local supply chain ecosystem for the hydrogen value chain

New Delhi: Today, India largely relies on fossil fuels to meet its energy requirements – most of which are imported. Consequently, our nation incurs enormous expenses creating a financial strain and dependency on other countries for our energy needs. This is an undesirable predicament for a country that aspires to achieve remarkable economic growth and aims to become the world’s third largest economy by 2035. This, coupled with our commitment toward climate change and carbon footprint reduction, is driving us as a nation to explore and consider greener fuels that can be produced indigenously. This will help us in solving energy security and climate change issues simultaneously. Green Hydrogen is at the forefront of the green fuels and has gained widespread attention today. Although much has been written and spoken about the pros and cons of green hydrogen as a fuel, the need of the hour is to deliberate on how we make it a reality for India by creating a sustainable ecosystem.

Consumption

The adoption of a new fuel is a gradual process which is dependent on multiple factors such as economic viability, technical feasibility, performance and accessibility. For industrial applications that already use hydrogen in grey or blue form, technical feasibility is proven therefore the focus is on economics and accessibility. However, in applications such as mobility where hydrogen is a new entrant, technical feasibility is the starting point which is being worked upon and successfully demonstrated by various OEMs. The economics of fuel usage is dependent on the economics of the entire value chain. And in most cases, economics is favorably impacted by large-scale fuel production by leveraging economies of scale which in turn is derived from large-scale demand. Demand, on the other hand, has economics as a key driver. This leads to a chicken and egg problem!

Few ways in which this problem could be resolved on the demand side are:

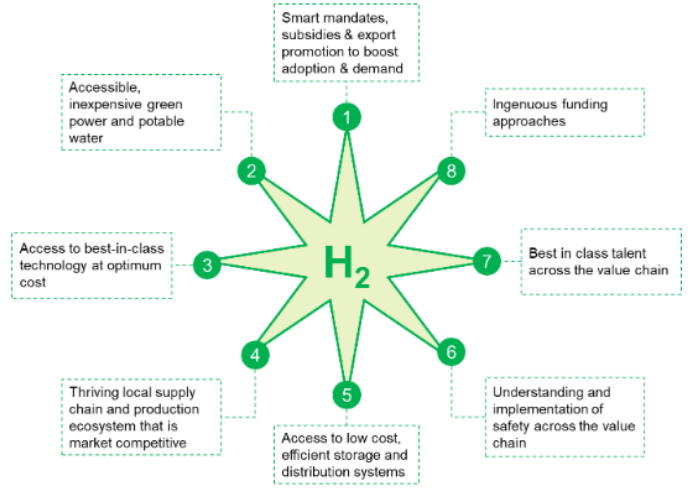

Bring in ‘smart mandates’ for green hydrogen usage in industries. These mandates are not just about setting a direct percentage of fuel usage. Instead, they specify a particular percentage usage if the cost of hydrogen is at a specific level. Until hydrogen costs are above this level, a viability gap funding is provided with a cap on the total corpus.

Boosting demand for hydrogen powered mobility especially in buses and commercial vehicles, which account for the largest consumption of diesel in the country, through FAME-like schemes.

Support in setting up export hubs for green hydrogen and hydrogen derivatives.

Forge government-to-government agreements with countries for supply of green hydrogen and its derivatives.

Generation

To achieve local generation of green hydrogen at a competitive cost requires four key factors to be in place – availability of inexpensive green power; availability of potable water; accessibility to the right technology; and large scale driven by huge demand which we addressed in the previous section.

India aims to achieve nearly 50 per cent of its power generation installed capacity from renewable energy (RE) sources by 2030. Many organizations in the solar industry have vertically integrated themselves into manufacturing of solar chips, modules, panels and other components, reducing the country’s reliance on other nations for the solar power value chain. This has led to a significant decline in solar prices in India. Additionally, the government has introduced the concept of ‘open access of renewable power’ and waived off inter-state transmission charges of solar power especially for green hydrogen production. All these initiatives have paved the way for access to low-cost RE power for the green hydrogen economy.

In terms of the availability of potable water, stoichiometrically, every unit of hydrogen generated needs nine units of water as input. Therefore, for an estimated 5 MMTPA of green hydrogen production in 2030 that the government envisions, the water requirement would be around 45-50 bn liters per year, which is equivalent to the water requirements of about two million people in India in 2030. This is quite a significant number. Few ways of addressing this issue could be:

– Evaluate how this volume of water can be additionally generated through methods like desalination of seawater. However, it is important to note that desalination will have a cost impact and needs to be addressed through incentives in the short term and design/process improvements in the mid term.

– Evaluate how the water consumption for water-intensive industries can be further optimized to release water for Green Hydrogen production.

India is currently heavily dependent on importing technology for electrolysis. Hence,to ensure a sustainable model for the future, India must pursue a two pronged strategy:

Encourage indigenous technology development: Since electrolyser technology is rapidly evolving, India must support indigenous technology development by creating an innovation/ incubation ecosystem where academia, start-ups and industries including global technology partners can collaborate to develop next-gen technology at lower cost and take it to market.

Incentivize global technology partners to set up base in the country either on their own or through partnerships with Indian firms: Firstly, a robust IP protection ecosystem needs to be provided in the country so that global technology players feel safe to partner with Indian firms without the fear of their IP being infringed. This will also facilitate joint development of IP in the mid to long term.

Next, there is a need to create a robust local supply chain ecosystem for the hydrogen value chain. India has demonstrated its strength in developing supply chain ecosystems for various industries and is capable of doing so in the case of hydrogen as well. While this ecosystem would organically develop over a period of time, it will need to be consciously driven in the initial years. This is an essential aspect for India to compete with the likes of China, which have more evolved Hydrogen supply chain ecosystems making them the preferred destination for global players today. The lack of such an ecosystem could deter investments into the country.

Lastly, with countries such as the US and many European nations providing incentives for setting up Green Hydrogen production facilities, India also needs to look at providing similar incentives through schemes such as PLI (Production Linked Incentives) to ensure that India features among the top investment destinations for global players.

Storage and distribution

In most cases, green hydrogen is being used as ‘stored RE power’ that can be used to regenerate power whenever and wherever needed. Therefore, storage of green hydrogen becomes a critical aspect. Options exist for storing hydrogen in physical forms such as gas, liquid, adsorbate or in chemical forms such as ammonia, and a lot of R&D and technology work is ongoing in this area. The distribution of hydrogen will depend on the level of centralization needed in production which will need to evolve over time, considering access to input resources and the need for proximity to points of consumption. It is important to note that both storage and distribution are key contributors to the cost and availability of hydrogen and, therefore, must have a high degree of localisation to the extent possible.

Safety

Safety is a critical aspect underlying all the aforementioned aspects of the hydrogen economy. With newer application areas emerging for green hydrogen and larger scale production, storage and distribution systems being envisioned, the safety of hydrogen must be well-studied, tested and implemented. Initiatives such as hydrogen valleys could be leveraged for this purpose.The higher the perceived safety risks associated with hydrogen, the lower the adoption rates are likely to be.

Talent

Last but not the least, India can emerge as a global hub for hydrogen only if it can successfully attract, develop and retain talent across the entire value chain including technology, suppy chain, operations and more.Some of the initiatives here could be:

– Encouraging global players to set up training or upskilling centers either through their own local set-ups or through partnerships with Indian entities in the country to upskill local talent.

– Supporting or sponsoring training programs for local talent in the green hydrogen space outside the country with reputed global players and institutes.

– Provide enriching career development options to attract global talent and retain local talent.

– Provide incentives for research and opportunities for incubation of new ideas.

– Offer specialized courses in hydrogen technology to develop a skilled workforce for the future,

Funding

While a lot many interventions have been suggested in this article, a key requirement for most of them is funding. It would be impractical to assume that all the funding requirements for building and sustaining the green hydrogen economy is the sole responsibility of the government. Given the constraints they face in allocating a finite corpus of money toward running the country, driving growth and addressing basic challenges such as poverty, education, health – innovative ways of funding these interventions through participation of government, industry, academia, global entities, etc, must be explored.

In summary, we need an ‘Octagram model’ for sustainable hydrogen economy as shown below:

[This piece was written exclusively for ETEnergyWorld by Subramanian Chidambaran, Strategy leader, Cummins India]

https://energy.economictimes.indiatimes.com/amp/news/renewable/opinion-exploring-the-path-to-a-sustainable-hydrogen-future-in-india/98535713